.png)

Motor claims management that earns its place in the P&L

Axxion manages the full motor claims lifecycle — from first notification through repair coordination, quality control, and settlement. Lower repair costs, faster cycle times, and an operation that is audit-ready from day one.

%201.png)

Six challenges all UAE motor insurers recognize

These six frustrations surface in every conversation with claims and executive leadership at UAE carriers. The details vary by insurer; the pattern does not.

Claims costs

Repair costs are structurally out of control. Parts inflation, labor rate creep, and a growing share of technology-heavy vehicles compound the problem year on year, drifting up faster than pricing can absorb.

Rising average severity, frequent exceptions, and budget surprises mid-year have become standard. Most insurers lack real-time visibility into cost drivers at the repair-line level, so corrective action arrives after the loss ratio has already moved.The other five blocks are cleared as written. All six are ready for the site.

Reserving accuracy

Reserving accuracy is weak, leading to P&L volatility and quarter-end surprises. Initial estimates are set with incomplete information and rarely updated as the claim develops, creating a gap that widens through the lifecycle.

Reserve strengthening exercises, surprises at quarter close, and inconsistent assessment quality erode confidence in the technical result. Actuarial teams spend more time explaining variance than preventing it.

Leakage

Leakage is real but invisible, insurers suspect it exists but cannot prove where it happens or quantify its scale. Without granular, structured data at the repair-line level, the gap between what should be paid and what is paid stays hidden in aggregated numbers.

Suspicions without evidence, internal audits that find issues late, and rework loops are symptoms of a broken feedback mechanism. By the time leakage surfaces, the money is already out the door and the pattern has repeated.

Data quality

Claims data is unreliable for decision-making — every team has a different version of the truth. Underwriting, claims, and finance pull numbers from separate systems and reconcile them manually, if at all.

Conflicting figures across departments, "Excel truth," and no single source of structured claims data make portfolio steering a guessing exercise. Decisions about pricing, reserving, and network management end up built on whatever spreadsheet was updated last.

Customer experience

NPS is dragged down by the claims experience, not by the insurance product itself. Policyholders judge their insurer at the moment of the claim, and that moment is where most carriers perform worst.

Complaints about delays, poor updates, and workshop disputes drive policyholder churn at renewal — often before the insurer knows there was a problem. The cost of acquiring a replacement customer runs at multiples of what a competent claims process would have cost to retain the original one.

Expense ratio

Claims administration cost per claim is too high, driven by manual processes and rework at every stage of the lifecycle. Each additional system, handoff, and approval layer adds cost without adding accuracy or speed.

High headcount growth, overtime, outsourcing creep, and duplicate data entry across systems are symptoms, not root causes. The underlying problem is a claims operation designed around paper and people rather than structured data and automation.

The insurers that will lead the GCC market specially Saudi Arabia are those that treat claims not just as a cost center but as a strategic capability combining intelligence digital infrastructure, smart outsourcing, and strong governance to stay agile under pressure.

Everyting changes when Axxion manages the claims operation

Every benefit traces back to one structural change: an independent, compliance-grade operation sitting between the insurer and the repair chain, with the data infrastructure to prove what happened and what it cost.

Lower repair costs

Repair pricing verified against independent market benchmarks before every authorization. Parts sourced through governed channels. Workshops paid the actual repair cost, not an inflated estimate — above-normal margins are removed from the chain.

Parts priced against independent market database before every authorization

Bulk procurement through predictive forecasting reduces unit cost

Cost curve shifts downward across repair categories as the data set grows

Fraud and leakage control

A digital audit trail runs from first notification through to vehicle return. No financial relationship exists between the claims handler and the workshop. Every cost element is verified, and anomalous patterns are flagged automatically.

Segregation of duties between assessment and repair

System-level safeguards against collusion

Suspicious cost profiles and claim frequencies surfaced in realtime

Faster cycle times

Built-in SLAs enforce discipline at every stage of the pipeline. Smart triage routes simple claims to fast-track resolution. Milestone tracking means delays are caught early, not discovered at settlement.

Seven-stage pipeline with time gates at each transition

Automated triage reduces manual touchpoints by routing simple claims to fast-track resolution

Shorter cycles directly reduce rental, storage, and ancillary costs

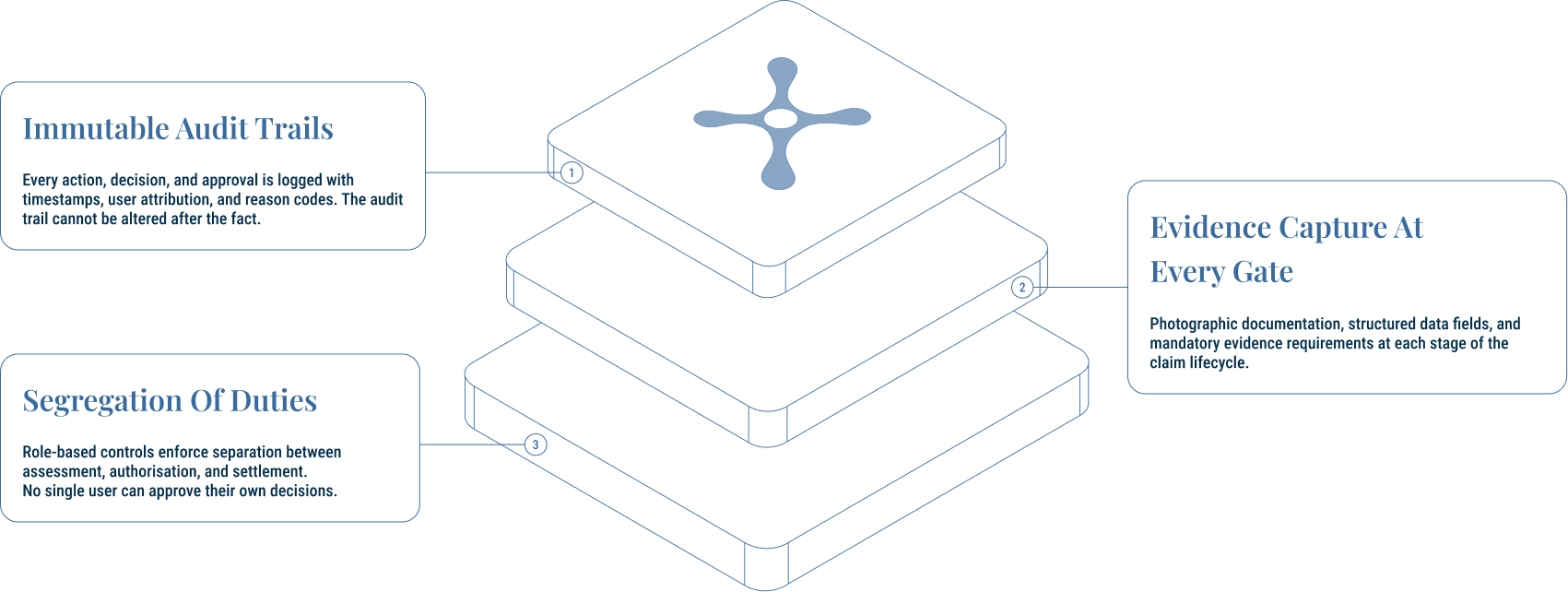

Transparency &auditability

Full evidence trail from notification to final invoice: itemized cost breakdowns, before-and-after repair images, workshop performance data, and standardized reason codes for every decision. Compliance is built into the workflow, not added after the fact.

Immutable audit trail satisfies CBUAE expectations

Consistent documentation replaces ad-hoc record keeping

Disputes drop when every decision is documented and defensible

Structured claims data

Granular, standardized repair data returned for every claim processed — usable directly for underwriting, actuarial analysis, and pricing. Burning cost by make, model, and year feeds reserving and fraud detection. Cross-carrier benchmarks become available for the first time in the UAE market.

Granular, standardized repair data returned for every claim processed — usable directly for underwriting, actuarial analysis, and pricing. Burning cost data by make, model, and year feeds reserving models and fraud detection.

As the portfolio grows, cross-carrier benchmarks become available that do not currently exist in the UAE market.

Better policyholder experience

Policyholders receive real-time status updates from notification through to vehicle return. Workshops are selected on capability and quality, not opaque arrangements. Repair quality is verified with pre-and-post documentation and sign-off. The claims experience becomes a retention driver rather than a complaint generator.

Transparent communication throughout the claim

Verified repair quality with documented QC sign-off

Claims experience differentiates the insurer in a crowded market

Inter-insurer claims settlement acceleration

Validated settlement claim data is prepared automatically upon repair completion — structured, audit-ready, and formatted for submission to the CBUAE inter-insurer settlement platform. Higher data quality reduces disputes and rejection rates between carriers, compressing settlement cycles from months to days.

Two service lines, one accountable partner

Axxion offers repair management and claims management as standalone or combined services. Both run on the same governed infrastructure with full audit trails, cost benchmarks, and quality gates.

Claims

Management

Full claims lifecycle from intake through validation, fraud screening, and closure. Axxion acts as a single accountable operations partner, removing administrative burden from the insurer while improving loss ratios and policyholder experience.

Scope: customer service, document management, reserving, claims administration, reconciliation, third-party recoveries, and supplementary staffing.

Repair

Management

End-to-end management of motor repairs: workshop selection, cost benchmarking, parts governance, and post-repair quality control. The insurer gets lower average repair costs, faster turnaround, and transparency that makes fraud visible rather than suspected.

Scope: damage assessment, cost estimation, triage and workshop allocation, repair coordination, parts sourcing and pricing control, and quality inspection.

4-Gate Quality And Cost Control

Axxion's 4-gate defense mechanism enforces strict adherence to compliance and cost containment measures. No gate can be crossed without proper documentation.

CLAIMS INTAKE / FNOL

Gate 1: Eligibility & Fraud

The claim is verified as payable before the vehicle moves or a repairer is engaged

What this gate catches:

Coverage & exclusions: non-covered events, partial cover, deductible implications, policy conditions,endorsements, exclusions

Eligibility gaps: expired policy, wrong driver, missing documents, non matching details

Fraud red flags: inconsistent accident narrative, document anomalies,repeated claimant/vehicle patterns,suspicious timing, staged-loss indicators

PRE-ESTIMATE ROUTING

Gate 2: Triage Protocol

Control where the car goes before it moves, based on car and damage

What this gate catches:

Misrouted repairs: drivable + minor damage not sent to quick repair partners, unnecessary agency referrals

Network inefficiency: underperforming workshops, poor cycle times, above benchmark costs, no capacity-aware assignment

Specialist mismatches: EV/ADAS/structural work sent to uncertified repairers, high-value vehicles in low-capability shops, warranty sensitive repairs

ESTIMATE CONTROL

Gate 3: Intervention

Audit and challenge every estimate before authorization

What this gate catches:

Labor inflation: excessive hours, duplicated operations, non-standard repair methods, uncapped paint and material charges

Replace-over-repair bias: parts replaced when repairable, unnecessary strip-downs, inflated panel counts, unjustified add-ons

Supplement abuse: repeat top-ups without evidence, scope creep after approval, missing documentation, noncompliant repair-vs-replace decisions

PARTS CONTROL

Gate 4: Spareparts Supply

Parts sourcing is governed so the workshop cannot inflate pricing

What this gate catches:

Price leakage: unapproved or undisclosed supplier markups, inflated parts pricing, no benchmarking against market rates

Sourcing non-compliance: OEM parts used where approved alternatives exist, by passed preferred suppliers, unauthorized parts substitutions

Billing irregularities: duplicate parts charges, unused parts not returned, phantom line items, parts invoiced but not fitted to vehicle

Compliance built into the operation, not bolted on

The CBUAE compliance horizon to September 2026 requires execution-based compliance: controls embedded in systems, not documented in binders. Axxion's workflows are designed so that compliance is a by-product of how claims are processed.

How Axxion proves the value

Axxion does not ask insurers to take improvements on faith. The model is built around measurable proof, starting with a shadow-mode pilot that runs alongside existing operations.

Savings methodology

Savings are measured against the insurer's own historic paid baseline for a comparable claims mix. Every savings claim is tied to a specific lever: labour rates, paint and materials, parts procurement, supplement control, or cycle time reduction. The methodology is documented, the baselines are agreed upfront, and the results are auditable.

Proof-pilots

Pilots run for 12 weeks across a defined claim set. Axxion processes claims in parallel with the insurer's existing operation, producing a direct comparison on cost, cycle time, auditability, and quality outcomes.

The output includes distribution metrics across the portfolio, outlier containment data, recommended confidence thresholds, and a documented exception log. No disruption to the live operation, no commitment beyond the pilot scope.

Pilot deliverables

Cost breakdown by repair category

Parts, labour, paint, and materials separated by vehicle segment

Variance analysis

Axxion benchmarks vs insurer's current repair cost baseline

Exception governance log

Every deviation documented with reason codes and approvals

Cycle time comparison

FNOL-to-settlement against existing operation

Audit trail sample

Complete decision documentation for sample claims